Just moved to Switzerland? You have to choose a health insurance. An insured resident who is currently suffering from rising premiums? In order to reduce your premium you need to compare offers.

It is true that health insurance premiums are expensive. Health insurance costs are important in the budget of Swiss families. Health insurance company plans are complex.

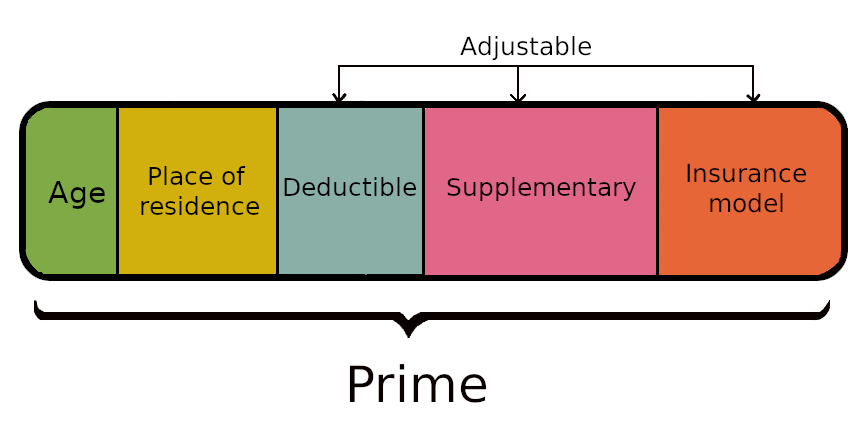

The cost of a premium is composed of 5 elements. Three of them are ‘adjustable’:

Age is something we cannot control. Apart from relocating, the place of residence is difficult to change. These two elements are rigid. In order to tailor your health insurance to your needs, the variables that can be adjusted are the deductible, the supplementary insurance and the insurance model.

To have the best health insurance, you need a method.

The choice of health insurance is a trade-off between the cost of the premium you are prepared to pay, the expected reimbursements and the desired level of care.

These are the 4 steps to find the most suitable health insurance for your needs, at the best price.

Step 1 – Choose your deductible

To have the best premium quote, the first adjustable block is the deductible. The premium is the amount paid each month. The deductible is the annual amount you pay before your health costs are reimbursed.

The higher the deductible – the lower the premiums. If you are not often ill, it is in your interest to choose a high deductible.

Choosing a high deductible means that you need to have a minimum amount of savings to cover the first expenses. For example, if you set your deductible at CHF 2,500, this means that you will have to pay CHF 2,500 before you start to be reimbursed for your medical expenses.

You should also bear in mind that once you have reached this deductible, you would still have to contribute 10% of the costs. Up to a cumulative total of CHF 700 per year, reimbursements are made at 90%. This is called the copayment. There is no copayment for children. Above the CHF 700 copayment, the LAMal benefits are reimbursed at 100%.

Step 2 – Choose your care package (supplementary)

The second adjustable block is supplementary health insurance. It covers services that are not reimbursed by the basic LAMal. It also allows access to ‘top up’ care that is not covered by the basic LAMal.

Unlike basic insurance, supplementary insurance is optional in Switzerland. The most obvious way to lower your LAMal premiums is therefore not to join a supplementary insurance plan.

However, it is important to bear in mind that the Swiss compulsory health care system is limited in its coverage. Not having supplementary insurance means running a financial risk if you need expensive care. For example, optical and dental services (excluding children’s orthodontics) are not covered by the basic LAMal compulsory health insurance scheme.

In many cases, supplementary insurance is necessary. If you fall into one of the following categories, we recommend that you take a look at the range of supplementary insurance.

Prioritising preventive medicine

Prevention is better than cure. Supplementary health insurance allows you to undergo preventive examinations and reimburses many alternative medicines.

It is true that supplementary insurance increases slightly the cost of your premiums. However, by reacting in advance, by favouring mild treatments as early as possible it can help to preserve your health. Therefore likely saving you a lot of money in the long run.

I need a wider range of care

The Swiss health system’s coverage is good but limited. Needs that may seem fundamental are not reimbursed by the basic insurance. This is the case for additional pregnancy tests, optical and dental expenses, etc.

If you wish to extend the range of care covered for services that you consider essential, we advise you to study the offers of supplementary insurance.

I need specialists and rapid referral

If you want to be taken care of quickly for a consultation or an operation, or if you want to choose your own specialist, you need a supplementary health insurance scheme.

Patients who wish to confirm the opinion of the first doctor before embarking on a heavy therapeutic treatment also increasingly request a second opinion. The complexity of medical advice is challenging, a second opinion helps to empower the patient

I would like ‘comfort’ service care

Private or semi-private health insurance entitles you to wellbeing benefits. The hospital stay can be in a single or double room. Being alone with your baby is particularly appreciated after childbirth, as is being able to sleep in the room of an eventual hospitalisation of your child.

Services that facilitate daily organisation are also offered. These include childcare for sick parents or sick children, and nursery services.

Supplementary insurance – An investment for the future

If you decide not to take out supplementary insurance in order to reduce your health insurance premiums, don’t forget to consider the long term.

Since supplementary insurance is optional, the insurance companies can refuse to accept you on the basis of your health questionnaire.

It is therefore advisable not to delay taking out supplementary insurance. Your medical history could make access to supplementary insurance more difficult.

Step 3 – Reduce your premium through alternative models and the ‘Tiers-Garant’ system

The third adjustable block for reducing health premiums is the alternative models.

These are constraints, additional conditions that are accepted in order to obtain reductions. Alternative models are designed to reduce the costs of basic insurance under the LAMal, while others are designed to reduce the costs of supplementary insurance.

There are also insurances that allow you to reduce your premiums by paying out of your own pocket for health care services and medication before being reimbursed by the health insurance company. This is known as the ‘Tiers-Garant’ system.

Alternative models for basic insurance

The best-known alternative model is the family doctor. By agreeing to start their treatment with a family doctor, the insured person benefits from a reduction in their LAMal premiums.

Another example is telemedicine. By promoting remote consultations, you participate in the digitalisation of medicine and benefit from a reduction in your premiums.

Alternative models of supplementary insurance

The logic of alternative models is the same for supplementary health insurance. For example, the ‘Flex’ model gives policyholders the possibility to choose on an ad hoc basis whether they want to access ‘semi-private’ or ‘private’ treatment. They can make this choice for a particular treatment. They will then have to pay a deductible

Look out for family discounts offered by supplementary insurance.

The ‘Tiers-Garant’ reimbursement system

The ‘Tiers-Garant’ system is a method of reimbursing health care services. Under the ‘Tiers-Payant’ system, the insurance company pays directly for the cost of medicines and health care services. Instead of paying the health care provider, the insured person presents the health insurance card. In contrast, in the ‘Tiers-Garant’ system, the insured person must pay for his or her health care services before being reimbursed by the insurance company.

To reduce the cost of insurance premiums, you can choose an insurance policy that offers ‘Tiers-Garant’ cover. Be aware, however, that this requires savings. You will have to pay out-of-pocket for health care costs before the health insurance fund reimburses you (depending on the cover of your insurance contract).

Step 4 – Choose your health insurer

You now know how to adjust and reduce your premiums. Test your preferences for deductibles, supplementary insurance and insurance models on our insurance comparison tool.

You can easily and quickly find the right insurance for your needs. You will automatically receive an initial offer to study at your leisure.

This initial feedback can then be refined with our advisor. The aim is to find the best-priced insurance that perfectly matches your personal situation and needs. This is how you can make the right savings on a health insurance premium.

Choosing your health insurance

Helvicare will support you during the 4 steps of the process.10,000 customers have already discovered the quality of helvicare’s support.